All personal property located in Currituck County that is used by or in conjunction with a business; or is used for the production of income is subject to local property taxes in Currituck County.

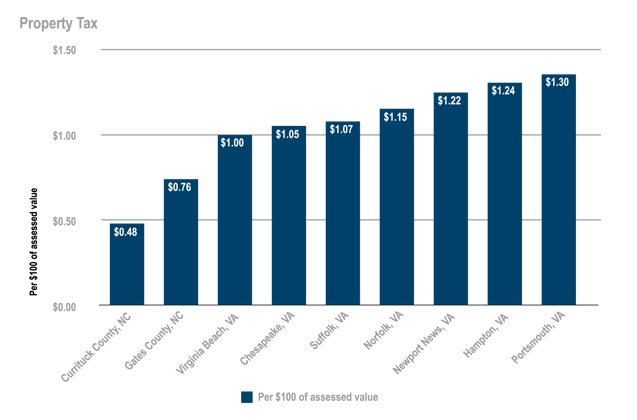

The current property tax rate for Currituck County is $.48 per $100 of assessed value.

Owners of such property are required by law to submit an annual personal property listing with the County Assessor during the listing period of January 1 - February 15.

Extensions for listing can be granted until April 15th if a written request is submitted to the Assessor by February 15. There is penalty for failing to submit the required annual listing.

For additional information contact the Currituck County Tax Department at (252) 232-3005.

Certain taxes must be withheld from employee wages and remitted to the appropriate government agency.

These include state and federal income taxes and FICA (Social Security).

The State of North Carolina requires that every new employer complete and file with the North Carolina Department of Revenue an application for a North Carolina withholding identification number.

In addition, the federal government requires that every employer who pays wages to one or more employees file an application for an employer identification number with the Internal Revenue Service.

You may hear these numbers often referred to as Tax ID Number or Taxpayer ID Number.

To register with the State of North Carolina, you must complete an Application for Withholding Identification Number (Form AS/RP1) (available at BLIO) and submit it to:

North Carolina Department of Revenue

PO Box 25000

Raleigh, North Carolina 27640

919-733-4626

To register with the federal government, Application for Employer Identification Number (Form SS-4) (available at BLIO), should be filed with:

Internal Revenue Service Center

Attn. Entity Control

Memphis, Tennessee 37501

As a public service, the Internal Revenue Service will assemble and forward to you a tax information kit that fits your particular business situation. The kit includes forms and publications that apply solely to federal taxes.

To obtain this information, contact the IRS at 1-800-829-3676 or their website, www.irs.gov, and request:

For more information regarding Federal Employer Identification Numbers, read Understanding Your EIN (Publication 1635).